Up to date on October fifth, 2023 through Aristofanis Papadatos

W.W. Grainger, Inc. (GWW) just lately larger its dividend for the 52nd consecutive yr. This implies Grainger has a place within the unique record of Dividend Kings. The Dividend Kings have raised their dividend payouts for no less than 50 years.

We consider high quality dividend enlargement shares just like the Dividend Kings are sexy for long-term traders. Because of this, we compiled a complete record of all Dividend Kings.

You’ll obtain the total record of Dividend Kings, plus necessary monetary metrics equivalent to dividend yields and price-to-earnings ratios, through clicking at the hyperlink beneath:

Grainger has maintained its Dividend King standing because of its awesome place in its business. Its aggressive benefits have fueled the corporate’s long-term enlargement.

As we see endured enlargement within the business-to-business vendors of the upkeep, restore, and operations (“MRO”) provides business, Grainger must continue to grow its dividend for lots of extra years.

On this article, we can talk about the enterprise style of Grainger, its enlargement catalysts, and its anticipated returns.

Industry Assessment

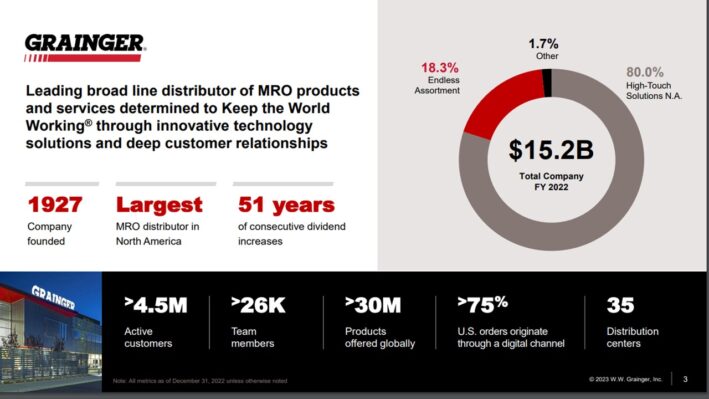

W.W. Grainger, headquartered in Lake Wooded area, IL, is without doubt one of the global’s biggest business-to-business provide vendors of upkeep, restore, and operations (“MRO”).

The corporate used to be based in 1927 and generated gross sales of $15 billion in 2022. Grainger trades with a marketplace capitalization of $35 billion. Grainger is a member of the Dividend Aristocrats Index and the Dividend Kings.

Grainger has greater than 4.5 million energetic shoppers, with greater than 30 million merchandise introduced globally.

Supply: Investor Presentation

It has additionally adjusted unexpectedly to the increase of e-commerce, as greater than 75% of its orders within the U.S. are positioned by way of virtual channels.

On July twenty seventh 2023, the corporate reported its second-quarter effects. Earnings grew 9% over the prior yr’s quarter, essentially because of 9.9% gross sales enlargement of Prime-Tech Answers amid subject matter payment hikes and endured quantity beneficial properties throughout all geographies.

The Never-ending Collection section additionally carried out neatly, with its gross sales rising through 10% on an adjusted foundation, pushed through new visitor acquisition around the section in addition to undertaking visitor enlargement.

Income grew 26.5% because of sturdy gross sales enlargement and a spread in gross margin and running margin through 170 and 190 foundation issues, respectively. Income consistent with percentage grew 29%, in part assisted through a discounted percentage depend.

In accordance with sturdy effects to this point in 2023 and no indicators of fatigue at the horizon, Grainger’s control workforce raised its full-year steerage for revenue consistent with percentage from $34.25-$36.75 to $35.00-$36.75.

Enlargement Possibilities

Grainger has grown its revenue consistent with percentage at an 11.2% moderate annual compound price between 2013 and 2022. This consequence used to be pushed through 5.5% annual income enlargement, an increasing benefit margin, and a three.3% moderate annual lower of the percentage depend.

Income consistent with percentage diminished 6% in 2020 because of the pandemic, from $17.29 in 2019 to $16.18. Any such small lower right through a fierce recession is indisputably sufficient and confirms the resilience of the corporate to downturns. Even higher, the corporate has recovered strongly from the pandemic, with document leads to 2021 and 2022. The corporate is on course for any other document in revenue consistent with percentage this yr.

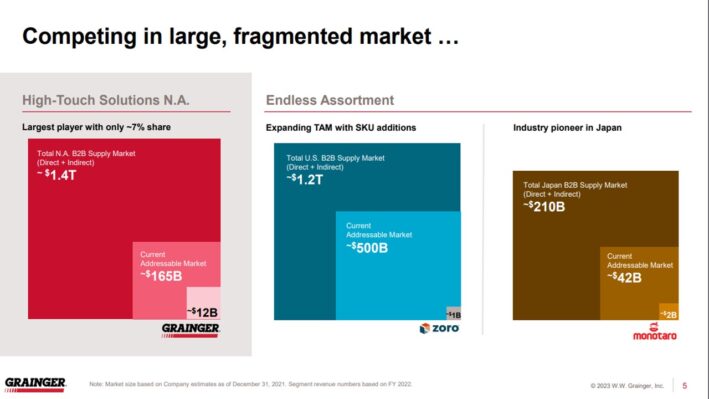

Additionally, Grainger has abundant room for long term enlargement. It’s the biggest participant in Prime-Tech Answers however has a marketplace percentage of most effective 7% within the North American marketplace.

Supply: Investor Presentation

Grainger additionally has quite a few room to develop its Never-ending Collection enterprise. The corporate is increasing its addressable marketplace with new merchandise and new visitor segments.

Additionally, the corporate will deepen visitor relationships thru service-based choices, which must lend a hand building up same-customer gross sales and general income.

Moreover, Grainger expects to spend $750-$850 million on percentage repurchases this yr. It’s thus prone to cut back its percentage depend through about 2.3% this yr. Proportion repurchases will proceed to lend a hand force revenue enlargement, as the corporate has decreased its percentage depend through a median price of three.3% consistent with yr since 2013.

General, we think Grainger to develop its revenue consistent with percentage through 6.5% consistent with yr over the following 5 years.

Aggressive Benefits & Recession Efficiency

Grainger’s most important aggressive merit is its sturdy place as an business chief in MRO merchandise. We consider that the corporate has a forged skill to battle off pressures from new (i.e., Amazon) and present companies within the MRO marketplace.

This exclusivity is constructed through forged provider relationships. As Grainger is the most important MRO commercial distributor in North The united states, it advantages from volume-based reductions and different gross sales incentives, which might be not possible through smaller vendors.

Those aggressive benefits give you the corporate with constant enlargement, even right through financial downturns. Grainger grew revenue right through the Nice Recession.

Grainger’s earnings-per-share right through the recession are as follows:

- 2007 adjusted earnings-per-share: $4.94

- 2008 adjusted earnings-per-share: $6.04 (22% building up)

- 2009 adjusted earnings-per-share: $5.25 (13% decline)

- 2010 adjusted earnings-per-share: $6.80 (30% building up)

This enlargement right through the Nice Recession speaks volumes in regards to the corporate’s resilience to financial downturns. As discussed above, the corporate carried out neatly right through the COVID-19 pandemic, with only a 6% revenue decline in 2020.

General, the corporate sports activities an A+ credit standing from S&P with a internet leverage ratio of one.0, which may be very forged. Thus, Grainger has the steadiness sheet power to resist any other recession.

Valuation & Anticipated Returns

We think Grainger to earn $35.88 consistent with percentage this yr. Because of this, the inventory is lately buying and selling at a price-to-earnings ratio of nineteen.1.

Over the last decade, the stocks of Grainger have traded with a median price-to-earnings ratio of nineteen.4. We’re the usage of 18.0 instances revenue as a good worth baseline, taking into consideration a quite slower anticipated enlargement price and a emerging price surroundings.

Because of this, we view the inventory as quite puffed up.

If the price-to-earnings ratio declines from 19.4 to 18.0 over the following 5 years, shareholder returns will likely be decreased through 1.2% consistent with yr.

On the other hand, dividends and earnings-per-share enlargement will spice up shareholder returns. Grainger has a present dividend yield of one.1%. Given additionally 6.5% annual enlargement of revenue consistent with percentage over the following 5 years, the inventory of Grainger is predicted to generate a median annual general go back of 6.2% over the following 5 years.

Ultimate Ideas

Grainger is a forged corporate with an incredible revenue and dividend enlargement historical past. It has grown its dividend for 52 consecutive years and therefore this is a slightly new member of the Dividend King record.

On the other hand, the stocks are buying and selling slightly upper than our honest worth estimate. Because of this, the full go back doable is available in at 6.2% consistent with yr over the following 5 years.

Although the full go back proposition does no longer seem compelling, the resilience of the corporate, its low dividend payout ratio (21%) and its spectacular dividend enlargement streak are notable. Nonetheless, stocks earn a dangle score on the present payment.

The next articles comprise shares with very lengthy dividend or company histories, ripe for variety for dividend enlargement traders:

Thank you for studying this text. Please ship any comments, corrections, or inquiries to toughen@suredividend.com.

{kind=link}